Profiles in Coverage: Indiana Check-Up Plan

![]()

Overview

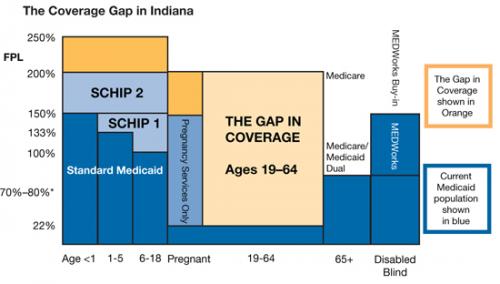

The Indiana Check-Up Plan, as passed by the Indiana General Assembly in 2007, contains several public and private reforms aimed at improving access to health insurance, funded through an increase in the cigarette tax. The centerpiece of the plan is the Healthy Indiana Plan (HIP), a high-deductible health plan (HDHP) coupled with a Health Savings-type Account (HSA) offered to low-income residents who have been without health insurance for six months, and earn less than 200 percent of the Federal Poverty Level (FPL) (i.e., $41,300 for a family of four in 2007). Uninsured individuals above 200 percent FPL can buy-in to the HIP plan at market rates.

HIP is financed by a 44-cent increase in the state’s cigarette tax, bringing Indiana’s total cigarette tax to 99.5 cents. This increase will provide coverage for 120,000 additional Hoosiers.

The Indiana Check-Up Plan legislation also:

- Provides tax credits to small businesses to establish Section 125 plans and wellness programs;

- Increases the age for dependent coverage to age 24;

- Funds tobacco cessation and immunization programs;

- Provides presumptive eligibility for pregnant women;

- Extends Medicaid coverage to pregnant women from 150 to 200 percent FPL;

- Allows the state to expand coverage for the State Children’s Health Insurance Program (SCHIP) from 200 to 300 percent FPL; and

- Increases reimbursement rates for current Medicaid providers.

While the HIP is the main coverage expansion, these other components also take important steps toward improving the overall health of Hoosiers and improving access to health care coverage.

The State Coverage Initiatives (SCI) program recently spoke with Mitchell Roob, Jr., secretary of the Indiana Family and Social Services Administration.

The State Coverage Initiatives (SCI) program recently spoke with Mitchell Roob, Jr., secretary of the Indiana Family and Social Services Administration.

Program Overview

Q. Can you tell us about the origin of the Indiana Check-Up Plan?

In 2006, Indiana Governor Mitch Daniels and the Indiana General Assembly asked us to create a health plan for the working poor and chronically uninsured. Our obstacles to a large degree were no more challenging than what other states are facing in this regard. The state had no successful effort to address uninsured adults since the inception of the Medicaid program in the 1960s, and consequently was ranked one of the worst in the nation for coverage. From 1999 to 2004, Indiana also had experienced the second largest decline in employer-sponsored insurance in the nation and had seen a 30 percent increase in the number of uninsured since 1990. Compounding the problem, Indiana also has extremely high rates of smoking and obesity and Hoosiers fall short in obtaining requisite preventive care as compared to national rates.

Despite these challenges, in a little over a year, Indiana passed legislation, negotiated a federal waiver, and implemented a plan to expand coverage to low-income uninsured residents.

Q. What challenges did you experience in developing such a program?

Looking back, our challenge was to construct a framework to promote personal responsibility, conscientious use of health care resources, and the prudent use of taxpayer dollars. Ultimately our greatest challenge was to create a plan that could garner not only broad bipartisan support, but that also could secure swift federal approval to obtain Medicaid funding.

Q. How did you get the support of important stakeholders in the state?

Through months of meetings, thousands of miles of travel, and hundreds of presentations, we sought to frame our argument by articulating that the financial burden of the uninsured resulted in increased premiums for the insured and thwarted price and quality transparency for all Hoosiers. We utilized data that demonstrated that 10 percent of each premium dollar paid by the insured population supported the cost of the uninsured due to cost-shifting by providers. We also explained that 67 percent of Indiana’s insured are low-income individuals earning less than 200 percent FPL, without any feasibly affordable health care option. These statistics made some form of a government subsidy inevitable. The data were irrefutable and most understood that doing nothing about the growing low-income uninsured would result in steeper premium increases and further exacerbate the imbalance of market forces.

In order to gain support for a coverage expansion, our plan had to ensure that it would encourage the prudent use of taxpayer dollars by the participants. We felt that participants must be partners with the state, and therefore must be aware of the cost of services they received in order to make responsible decisions about appropriate and medically necessary care.

Q. Can you explain the consumer-directed element that is part of the plan?

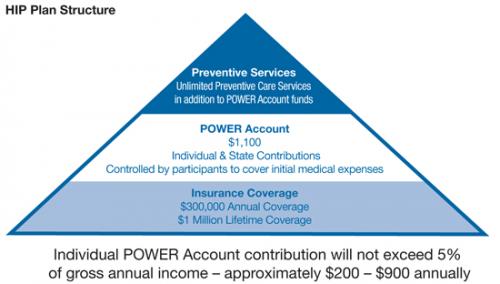

As we began to formulate the plan, Governor Daniels introduced the idea of using HDHPs and HSAs as a coverage vehicle. They promote the notion of consumerism and promise greater price transparency, competition, and quality. They not only encourage healthy lifestyles, but also provide individuals a financial incentive to seek information to make cost- and value-conscious health care decisions, which in turn increases pressure on providers to demonstrate value and quality. Since these mechanisms were very new and criticized for creating perverse incentives, especially for low-income individuals, to obtain needed care and critical preventive services, we had to develop a plan that would play off of the strength of HDHPs and HSAs, but could also be effective for vulnerable low-income populations under the Medicaid umbrella. With these parameters, the Healthy Indiana Plan with the Personal Wellness & Responsibility (POWER) Account was created.

Q. Can you describe how the POWER Account works?

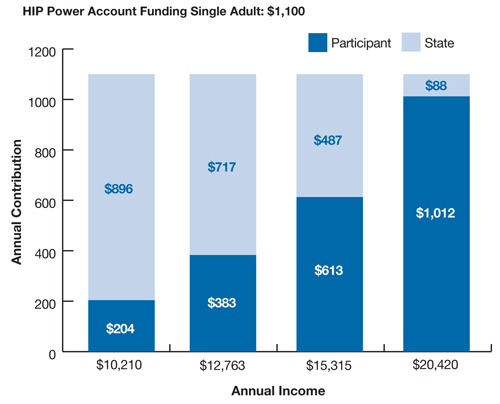

Modeled in the spirit of HSAs, the POWER Account is used to fund the $1,100 deductible required by HIP. Moving away from premiums and co-pays that are typically too low to incentivize collection by providers, HIP requires individuals to make mandatory monthly contributions to their POWER Account. After their monthly contribution, participants have no other cost-sharing requirement except for co-pays for non-emergency usage of the emergency room. While contributions are higher than traditional Medicaid premiums, participants have control over how these dollars are spent for eligible medical expenses. They become consumers with an incentive to demand price transparency and make decisions about how to obtain the best value for their purchase.

Q. Since early studies have indicated HDHPs/HSAs do not work well for low-income individuals because the deductibles were often not affordable and discouraged participants from obtaining necessary health care services, how did you address the skepticism about using them?

We created two mechanisms to specifically address these issues. First, recognizing that even after the required contributions many would still be unable to afford the $1,100 deductible, the HIP plan provides upfront subsides to the POWER Account to ensure that the account is fully funded to cover the deductible. Second, while we want participants to think carefully before utilizing health care, we did not want participants to apply this rationale to preventive health services. Originally, HIP was going to provide $500 of first-dollar coverage for preventive care, which the state broadly defined to include even smoking cessation and smoking patches in an effort to curb the state’s high rates of tobacco use. In the end, the result was better than what was outlined in the legislation. Due to successful competition between Anthem Blue Cross Blue Shield and MDWise with Americhoice, the two plans that won the state’s bid to offer the product chose to offer unlimited coverage for preventive care services, so the $500 threshold is not being used.

Q. How did you address the issue of POWER Account balances left over at end of year?

During the formative process, there was much debate about how to handle year-end POWER Account balances to reward cost-conscious behavior. Traditional HSAs allow account balances to roll over and are used to pay for future health care expenses. Because contributions are made on a pre-tax basis, there is an incentive to keep the money in the account to avoid penalties. Contributions made to the POWER Account, however, are not made on a pre-tax basis, as most low-income individuals would not benefit.

Many legislators wanted the balance to be paid back to the individual so he or she could purchase health care services not covered by the plan, such as dental care, or even allow participants to simply receive cash back, both of which are very attractive features for promoting healthy lifestyles and value and cost-conscious behavior. However, it seemed circular to pay out the balance and then require subsequent contributions. Many were also concerned about cash payments being used for non-health care items, especially if the payouts included state and federal monies.

In the end, we allowed the balance of the POWER Accounts to be used to offset required participant contributions in the following years. At the end of the year, the balance of the POWER Account will roll over to reduce the following year’s required contribution, if the participant has received their age-, gender-, and disease-specific preventive services. If they have not received these services, only their own, pro-rated contribution to the POWER Account will roll over, but the state’s contribution will be returned to the state. This design is intended to create an incentive for recipients to obtain appropriate preventive care and use services in a cost-conscious manner.

Q. How are the monthly contributions determined?

Required contributions range from 2 to 5 percent based on income, never exceeding $92 a month for an individual. Employers are also allowed to make contributions up to 50 percent of the individual required contribution. In order to prevent participants from obtaining temporary coverage, penalties are stiff for payment lapses. Participants have up to 60 days to make their contribution and are then terminated and cannot reapply for 12 months.

Q. How do participants manage their POWER Accounts?

Participants are responsible for managing their POWER Accounts and receive monthly statements for the account, as well as a summary of progress toward annual and lifetime limits ($300,000 annual coverage/$1 million lifetime coverage).

Q. What benefits are covered under the plan?

Benefits are comprehensive and include physician services, in-patient and out-patient hospital services, generic prescriptions if available, mental health and substance abuse treatment, and durable medical equipment (DME). Vision, dental, and chiropractic services are not covered. Maternity is not covered because it is covered by the Medicaid program.

Q. The potential fiscal impact of new coverage programs is always a difficult issue for legislators. How did you address this challenge?

The fiscal impact was of concern to everyone. No one wanted to create a program that could not be sustained over time. In order to address this, we designed an “anti-entitlement provision.” The legislation restricts the state from providing services “beyond the level of state appropriations authorized for the plan.” The provision contains the plan’s budget to the amount of revenues collected through the cigarette tax, and would require the state to adjust the program through either the number of enrollees or the benefits provided to stay within budget. This ensures that the program will not be a burden to future generations and that growth can be controlled and maintained. In reality, if there is growth in the program, legislators will likely be pressured to find additional funding to support growing enrollees and costs. Nevertheless, the implications of a non-entitlement program were enormous, as it gave many legislators the peace of mind to allow them to support the bill.

Q. One lesson that has become apparent with other state reforms that have passed in the last few years is that support has to come from both sides of the political aisle. Was this the case in Indiana?

The bill obtained bipartisan support to pass in our split legislature largely due to the efforts of both our Republican Senate sponsor and our Democratic House sponsor. They worked effectively together and their leadership reached across the aisle to colleagues who had long kept health care issues outside of partisanship. These relationships were further cemented by a passionate coalition of anti-smoking and health advocates who provided support and actively engaged in the dialogue. The mental health community, in particular, improved the plan by rallying for full mental health parity, which was included in the final version of the bill.

Q. How did hospitals and practitioners react to the bill?

Hospitals presented a special challenge for us. We knew that in order to secure federal funding and meet federal budget neutrality requirements, we would have to divert a portion of hospitals’ institutional entitlement in the form of their Disproportionate Share Hospital (DSH) funding to the new program. After making changes to the DSH program and other programs, the association that represents Indiana hospitals provided their full support. Practitioners were also initially reluctant to support the plan, as current Medicaid reimbursement rates had not been increased since 1993. In response, the legislature not only raised Medicaid rates, but also required the use of Medicare rates, instead of Medicaid rates, under the HIP plan to ensure an adequate delivery system for the new covered population.

Q. What role, if any, do employers have?

Employers may contribute up to 50 percent of the individual’s required contribution. We also have a program to facilitate payroll deduction for individual contributions, which requires the employer’s assistance.

Q. What was the greatest challenge in the negotiations with the Centers for Medicare and Medicaid Services (CMS)?

Perhaps the greatest challenge and most worthwhile exercise in our federal negotiations was in regard to childless adults. While funding is not available to cover all of the uninsured under 200 percent FPL, the legislation makes the program widely available and does not limit the program to specific categories such as parents of SCHIP-eligible children. Ultimately, we felt that only the federal Medicaid rules care whether a person is a parent or is a childless adult. If someone is low-income, uninsured, and willing to make the monthly contributions and play by the HIP rules, he or she should be allowed to participate — regardless of parental status. We should not value a parent over a childless adult. Medicaid laws, however, see this issue differently and budget neutrality rules thwarted our effort. In the end, coverage for childless adults was capped at 34,000 lives, leaving the remaining slots for parents of SCHIP-eligible children. However, CMS did give us permission to change eligibility requirements in the future. As our funding levels change, we can cap the program; however, individuals already enrolled in the program will be protected.

Q. What modifications had to be made to the original legislation in order to secure CMS approval?

CMS was clear that neither the employer’s nor the individual’s contributions to the POWER Account would be matched and that no federal dollars in the account could be paid out to individuals. The state was also unsuccessful in obtaining approval for a dental and vision rider program that would allow individuals to pay more than the required 5 percent contribution to obtain dental and/or vision coverage. We also had to lower the monthly contributions limit to accommodate co-pays and were limited in the amount of co-pays we could charge for emergency room use.

Q. How are you evaluating the effectiveness of the plan?

We have developed an evaluation plan that will examine claims data, membership files, use of the POWER Account, and utilization trends. The evaluation will also include a provider and member survey.

Q. What is the current enrollment in the program (number of businesses and/or covered lives)? What do you anticipate the enrollment to be at the end of this year and in the long term?

CMS approved the 1115b waiver in December of 2007, and by mid-January 2008, more than 17,000 individuals had applied. We have received more than 46,000 applications in less than five months and currently over 15,000 Hoosiers have been approved for coverage.

Q. Do you have any crowd-out provisions other than the requirement that an individual did not have insurance during the previous six months?

Yes — individuals cannot be eligible for employer-sponsored health insurance.

Q. How are you reaching the target population? What marketing and outreach has the state done to draw individuals to the program?

We have developed a series of TV, billboard, and radio ads that promote a toll-free number. We also developed a network of volunteer and community organizations, safety net providers, and hospitals throughout the state that have helped promote the program. The community engagement and a marketing campaign that features the Governor have been crucial to our marketing success.

Q. Have many participants lost coverage as a result of payment lapses?

At this time probably less than 10, but it is so early in the program that it is too early to tell the real impact of our personal responsibility requirements.

Q. Do you think the $1,100 is appropriate amount for those with chronic conditions?

The $1,100 deductible may in fact be too low for those persons with chronic conditions. Persons with chronic conditions will likely go through $1,100 very quickly. Because this is a Medicaid program, we are bound by the 5 percent out-of-pocket maximum imposed by CMS. Once participants spend the $1,100, they are not financially liable for services rendered during the rest of the year, as the state will cover all services.

As we gain more experience in the program, we will continue to evaluate the health status of participants to assess whether the deductible should be increased. By increasing the deductible, there would be greater financial incentives to complete requisite preventive care and to manage the larger POWER Account.

Q. Are you seeing any changes in the system as a result of the HIP program? Are any goals being explicitly set for institutions in the state?

With only five months into the program, it is too early to tell, but this is something that we will be evaluating.

Q. Despite being early in the implementation phase, are there areas that you would like to improve upon?

Absolutely. We wonder if there should be additional co-pays for those individuals not paying up to the 5 percent CMS limit to further encourage appropriate utilization as well as minimum contributions for all participants. Currently POWER Accounts contributions can only be made by the state, individuals, and employers. Perhaps health plans should be able to operate incentive programs, and make contributions to the Accounts as well. Interest in the overall HIP is high and it is likely that the amount of the cigarette tax may need to be revisited.

Q. What lessons have you learned from this process that should be considered by other state and national policymakers looking to successfully pass health reform?

- Private Market Solutions: Solutions to address the uninsured must work in tandem with the private market, and should not allow individuals to obtain services for free. All market consumers must play by the same rules and make some contributions toward their care. Government subsidies should be redirected to empower individuals to act as prudent consumers of health care. The fundamental Medicaid program must be reevaluated to encourage responsible behavior, rather than sustaining dependence and paternalism.

- Local Solutions: The face of the uninsured in each state is different. States must be empowered to develop local solutions. To make this successful, the federal waiver process must be overhauled to assist and support states, rather than to slow innovations.

- Finding a Champion: States looking to reform must identify a high-level local champion(s); one that not only has established relationships and the trust of the community, but also has access to the data and technical support to spearhead such efforts. The champion must also possess the political savvy to rally support from local leaders across vastly different philosophical and political backgrounds. Above all, the local champion must possess a tenacious determination to succeed.

- Never Let the Perfect Be the Impediment of the Good: HIP is pragmatic in both its design and approach. The plan includes multiple mechanisms to not only empower individuals to enter the health care marketplace, but to also promote personal responsibility and the prudent use of health care resources. It attracted wide bipartisan support because it provides a reasonable coverage option to the uninsured, while working in harmony with the private market for the currently insured.