State Fiscal Conditions Darken

![]()

After several years of fiscal stability, states are navigating a bleak economic landscape. Undoubtedly, declining state revenues will severely undermine future spending and coverage plans. As the impact of the nation’s worst financial crisis since the Great Depression ripples through state economies, many states are already experiencing difficulties. The collapse of the housing market and growing cost of energy have taken a toll on state revenues, creating budget gaps and the urgency for short-term borrowing.

States routinely borrow to meet short-term spending obligations, particularly given calendar fluctuations in incoming revenues; accordingly, lenders typically count on states to repay their loans.[i] In fall 2008, however, a slump in the credit markets caused lenders to restrict access to loans, causing many businesses and states to worry about their ability to borrow short-term cash. California and Massachusetts were the first states to raise the alarm that a credit freeze might jeopardize their short-term borrowing needs. Like others, these two states may need to turn to the federal government as a lender of last resort.

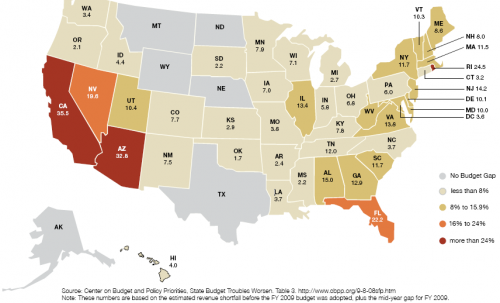

Even before the financial crisis, many states were facing budget deficits that forced them to raise taxes, cut spending, or both. In fact, in early 2008, 29 states had already confronted budget shortfalls totaling $48 billion as they prepared their fiscal year (FY) 2009 budgets.[ii] By December 2008, new mid-year budget gaps emerged, leading to budget gaps in at least 41 states and the District of Columbia, amounting to an estimated $43 billion shortfall, totaling 8.8 percent of state budgets.[iii] The projected gaps for fiscal year 2010 is 16.8 percent, based on states that are already reporting projections. Forecasters predict that these budget gaps will only worsen as states struggle with declining revenues.[iv]

By law, most states must balance their budgets. When the economy sours, states cannot run deficits and must close budget gaps by cutting expenditures, raising tax revenues, or drawing from rainy day funds or reserves. For many states, the worst financial crisis in recent times will mean layoffs and program cuts. Virginia is one such example. Faced with a $2.5 billion shortfall for its two-year budget, Virginia is laying off 570 state workers, leaving vacant an additional 800 unfilled positions, and instituting a hiring freeze. The state also plans to close several older correctional facilities and will reduce the budgets of higher education institutions by 5 or 7 percent. These cuts, however, address only a portion of the state’s budget gap, necessitating further spending reductions.[v]

Continue reading on: Medicaid Enrollment, Spending Set to Swell

[i] Johnson, N. “States Face Two Immediate Financial Issues: Short-Term Borrowing and Big Budget Deficits,” Center on Budget and Policy Priorities, October 7, 2008.

[ii] McNichol, E. and I.J. Lav op. cit.

[iii] Ibid.

[iv] Ibid.

[v] “Governor Kaine Announces Revenue Reforecast, Plan to Address Fiscal Year 2009 Shortfall,” Official Site of the Governor of Virginia, October 9, 2008.