State Reform Efforts Target Small Employers

![]()

Several state reforms have focused on assisting small employers’ efforts to provide access to health insurance. Between 2005 and 2008, at least 10 states enacted new programs to improve or increase coverage in the small group market.[i] Recent innovations include wellness plans, first-dollar coverage benefit design, and assistance with implementation of Section 125 plans. Other reforms include reinsurance, tax credits, and premium subsidies. This section explores some of the challenges in the small group market and highlights some of the new ideas being pioneered by states.

The Problem: Erosion of Small Group Coverage

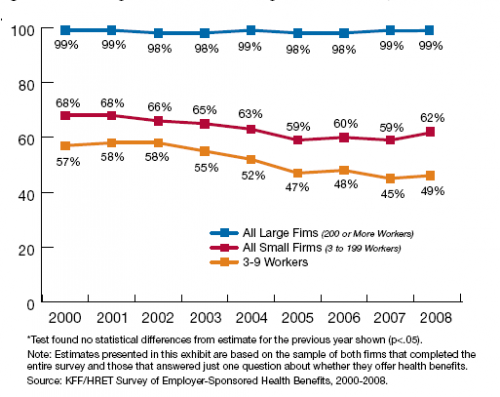

The continuing erosion of employer-sponsored insurance (ESI) and related increases in the number of uninsured explain much of the ongoing interest in reform of the small group market. While the percentage of large firms offering coverage has remained fairly constant at 98 or 99 percent of workers, the percentage of employers with fewer than 200 workers offering insurance fell from 68 percent in 2000 to 62 percent in 2008 as shown in Figure 7. Even fewer very small employers (three to nine employees) offer coverage; their offer rate fell from 57 to 49 percent.[ii] The loss of ESI, primarily driven by a drop in coverage among small firms, has been a major cause of falling coverage rates in the United States since 2000.[iii] More than 62 percent of uninsured adults work for small firms (100 or fewer employees) or are self-employed.[iv]

The lower rates of coverage in the small group market are attributable to several factors. First, those in the small group market face higher administrative costs because of the smaller pool of people across whom to spread the fixed costs of marketing, enrollment, and underwriting, thereby driving up per person premium costs.[v]

Figure: Percentage of All Firms Offering Health Benefits, 2000-2008

Second, premiums can change dramatically from year to year because of the health experience of one or two workers. Third, insurance plans often mark up premiums out of concern about year-to-year variation in health costs.[vi] Fourth, small firms tend to pay lower wages in general than large firms and operate on tighter margins, making it more difficult for them to offer comprehensive health insurance to workers.[vii],[viii]

Even among employers who continue to offer coverage, the trend is toward greater employee cost sharing. Under one definition of underinsurance,[ix] the increase in underinsurance was 60 percent between 2003 and 2007.[x] Those insured in the small group market have been particularly affected by this increase. In 2008 alone, the percentage of small business employees (3-199 employees) with a deductible more than $1,000 jumped from 16 to 35 percent.[xi]

Approaches to Coverage Expansion

To address the low and declining coverage rates among small businesses, states are turning to several approaches, including: 1) premium subsidies; 2) reinsurance; 3) restructured benefit design; 4) Section 125 plans; and 5) employer mandates. Several of the newer programs employ a combination of these approaches.

Premium Subsidies—Because affordability is one of the greatest obstacles to coverage, many states have enacted legislation to permit subsidization of employers willing to contribute to their workers’ health coverage. In effect, the state adds private dollars (from the employer and employee) to state funds as a cost-effective way to expand coverage. Nonetheless, states face several design questions when considering subsidies. Should the state subsidize coverage already sold in the market? Should it try to influence the benefit package? Should a state use Medicaid funds (which constrain benefit design options)? Should a state subsidize the premium through the tax code or through monthly payments? Should a state limit the plan to workers whose employers participate or should they open the plan to individuals as well? Should a state require a person to be uninsured for a given amount of time before qualifying for coverage? Table 1 demonstrates that states have answered these questions in a variety of ways.

Maryland offers a recent example of a program that combines a subsidy with other policy approaches. The Maryland Health Insurance Partnership is a premium subsidy program for small businesses (2 to 9 employees) that began enrollment in October 2008. The state offers a 50 percent subsidy for health insurance premiums; in return, the employer must establish a Section 125 plan to ensure that the premium is paid out of pre-tax earnings. (See page 52 for more information about Section 125 plans.) For a plan to be eligible, it must encourage wellness by providing employees with a health risk assessment and incentives for health-promoting activities, preventive care, and chronic care management.[xii] To qualify for the subsidy, the employer cannot have offered coverage in the last 12 months.

Reinsurance—Healthy New York is one of the oldest and largest state-based small group coverage programs. To lower costs for qualified individuals and small groups, the state: (1) reduced the benefit package and increased cost sharing; (2) provided care through limited networks that agreed to a reduced reimbursement; and (3) included a state-funded reinsurance program. Since enactment of the program, the state has enhanced the program’s attractiveness by offering additional choices of benefit packages. The Healthy New York plan costs about 40 percent less than average premiums in the small group market and two-thirds less than premiums in the individual market.[xiii]

The state covers 90 percent of the costs for an individual between $5,000 and $75,000.[xiv] To manage the costs of enrollees, New York retained the incentives for insurers by requiring enrollees to pay 10 percent of premiums between $5,000 and $75,000 and all additional costs above that threshold. Healthy New York has been operating since 2001 and covered about 153,000 enrollees as of fall 2008.

Restructured Benefit Design—Across the insurance market—in large businesses, public employee plans, and publicly funded coverage—purchasers are adopting strategies to promote wellness and improve health through an emphasis on prevention, primary care, and healthy lifestyle choices. These strategies are being applied to the small group market as well. In general, state policymakers are seeking to slow or reverse the trend in declining coverage rates in the small group market without resorting to the typical strategies of cutting benefits and increasing cost sharing. They believe that they can use the state’s regulatory power to encourage health plans to use strategies that would help enrollees become healthier, thus reducing underlying costs over time.

Rhode Island has been leading the way in promoting wellness plans in the small group market. They issued a request for proposals to carriers for a wellness product, indicating that the benefit package should emphasize preventive care and noting that the average premium for the plan could not exceed 10 percent of the state’s average annual wage, or $314 for single coverage (in 2007).[xv] Now that carriers have responded with benefit package proposals, the state is expected to meet its legislatively defined price point, reducing to approximately 20 to 25 percent below market rate the premiums for all small businesses. In 2008, the New Hampshire and Florida legislatures enacted similar initiatives. For more information on these initiatives, click here.

Benefit designs emphasizing first-dollar coverage, along the lines of benefit plans being offered in Tennessee and Arkansas, provide another strategy that merits consideration. Tennessee set guidelines during the procurement process for two state-sponsored products that require the successful carriers to emphasize preventive care at an average premium of $150 per member per month (2007 rates). After the state and the employer each contribute one-third of the total premium, individuals pay between $35 and $99 per month depending on age, tobacco use, and body weight. An annual limit of $25,000 per person applies, along with limits on hospitalization costs, prescription drugs, and physician visits. To participate, an employee must work for a low-wage firm that had not offered health coverage for at least six months. Once purchased, the coverage is portable and can even cover the individual during periods of unemployment. Subsequent expansion of the program applies to individuals working for large businesses who have been without health coverage for at least six months.

Advocates of Tennessee’s approach argue that low-income individuals are less worried about protecting their assets in the case of a catastrophic event and more interested in a policy that pays for routine care. Despite continuing concern about individuals who exceed benefit limits, the hope is that patients will receive the primary and preventive care that helps them avoid the need for expensive specialty or hospital care.

Both the Tennessee and Rhode Island reforms set a target price and asked insurers to bid on the services they could provide for that premium within certain parameters. These states are attempting to use their negotiating power to secure a better deal for enrollees.

Employer Mandate and Section 125 Plan Requirement—In 2006, Massachusetts began taking an aggressive approach by implementing a series of reforms that address both the individual (non-group) and small group markets. The reforms called for merging the state’s small group and individual markets; establishing the Health Connector (which is a clearinghouse of commercial insurance plans); requiring employers to offer a Section 125 plan (a tax shelter for premiums paid by employees); and imposing a penalty on employers with 11 or more full-time employees who fail to offer coverage to full-time workers. According to a recent survey of employers in the state, coverage in the small group market increased between 2007 and 2008 from 63 to 70 percent among employers with 3 to 10 workers and from 88 to 92 percent among employers with 11 to 50 workers.[xvi] While several reasons could explain the uptick in coverage—including the possibility that the state’s individual mandate caused higher demand among employees—it is still remarkable that Massachusetts has been able to counteract or possibly even reverse the national trend of declining coverage rates in the small group market.

Implementation and Evaluation—As states work on a range of strategies, they discover that even the most well-conceived policy interventions do not always achieve expected results if the interventions are not properly implemented and evaluated. Implementers should work closely with business groups to ensure that a program meets the needs of local businesses and that participation is simple. An effective marketing campaign requires reliance on many outlets for communication; a state cannot expect a program to succeed if the state does not promote it. Careful consideration should be given to the role of brokers in the program, as they are the traditional conduit for small businesses’ purchases of insurance and selection of insurance products.[xvii] Finally, states will not know if a program succeeds unless every program includes a strong evaluation component. Evaluation enables policymakers to recast programs midstream to address barriers and help ensure effectiveness.

Conclusion

A word of caution is in order about coverage expansion programs that target small businesses. Even “successful” programs have attracted only a small segment of the insurance market. It is difficult and expensive to engage small and often low-wage employers. A small employer may have only one or two uninsured workers, and those workers may or may not be interested in paying part of the premium for coverage. States have had greater success in enrolling large numbers of uninsured workers by targeting individuals, often with initiatives funded through Medicaid. However, if a state has set the more modest goal of achieving increased affordability, choice, and fairness for employers and employees in small firms, many of the policy options discussed above are worth consideration. The small group market is costly, unstable, and eroding, yet several tools are available to states to help employers offer health insurance to their employees.

[i] See Table 1and the new programs in Rhode Island, Florida, and New Hampshire described on page 57.

[ii] “Employer Health Benefits Annual Survey, 2008,” Kaiser Family Foundation and Health Research Education Trust, September 2008.

[iii] Holahan, J. and A. Cook. “The U.S. Economy and Changes in Health Coverage, 2000-2006,” Health Affairs, Vol. 27, No. 2, 2008, w135-w144.

[iv] Fronstin, P. “Sources of Health Insurance and Characteristics of the Uninsured: Analysis of the March 2005 Current Population Survey,” Issue Brief 287, November 2005. www.ebri.org/pdf/briefspdf/EBRI_IB_11-20051.pdf.

[v] Blumberg, L.J. and L.M. Nichols. “Why are So Many Americans Uninsured?” Health Policy and the Uninsured, C.G. McLaughlin, ed. Washington, DC: Urban Institute Press, 2004.

[vi] Cutler, D. “Market Failure in Small Group Health Insurance,” Working Paper No. 4879, Cambridge, MA: National Bureau of Economic Research, Inc., 1994.

[vii] Nichols, L.M. et al. Small Employers: Their Diversity and Health Insurance, Washington, DC: The Urban Institute, 1997.

[viii] Information in the preceding paragraph references comments and notes from a statement by Linda J. Blumberg to the U.S. House of Representatives Committee on Small Business, September 18, 2008.

[ix] (1) Out-of-pocket medical expenses for care amounted to 10 percent of income or more; (2) among low-income adults (below 200 percent of the Federal Poverty Level), medical expenses amounted to at least 5 percent of income; or (3) deductibles equaled or exceeded 5 percent of income.

[x] Schoen, C. et al. “How Many Are Underinsured? Trends among U.S. Adults, 2003 and 2007,” Health Affairs, Vol. 27, No. 4, pp. w298-w3099.

[xi] “Yearly Premiums for Family Health Coverage Rise to $12,680 in 2008, Up 5 Percent, as Many Workers Also Face Higher Deductibles,” Kaiser Family Foundation, press release, September 24, 2008. www.kff.org/newsroom/ehbs092408.cfm.

[xii] The Maryland Health Insurance Partnership Web site, www.mhcc.maryland.gov/partnership/

[xiii] Schwartz, K. “Reinsurance: How States Can Make Coverage More Affordable,” The Commonwealth Fund, 2005.www.commonwealthfund.org/publications/publications_show.htm?doc_id=286904.

[xiv] Ibid.

[xv] “Health Insurance Bulletin, Number 2007-1, Office of the Health Insurance Commissioner, State of Rhode Island; available at http://www.dbr.state.ri.us/documents/divisions/healthinsurance/070306%20Bulletin%202007-1.pdf;

[xvi] Gabel, J. R. et al. “After the Mandates: Massachusetts Employers Continue to Support Health Reform as More Firms Offer Coverage,” presentation slide 8, 2008. www.allhealth.org/briefingmaterials/GabelPresentation-1338.ppt#272,8.

[xvii] For a more thorough discussion of design and implementation features that promote enrollment in small business plans, see Volpel, A. et al. “Marketing State Insurance Coverage Programs: Experiences of Four States.” www.statecoverage.org/node/164.